Fill in Your Indiana Wh 4 Form

Similar forms

The Indiana WH-4 form is similar to the federal W-4 form, which is used by employees to determine the amount of federal income tax withholding from their paychecks. Both forms require employees to provide personal information, such as name and Social Security number, and allow them to claim exemptions based on their marital status and number of dependents. While the WH-4 focuses on Indiana state and county taxes, the W-4 pertains to federal tax obligations, making them complementary in the context of tax withholding.

Another document comparable to the Indiana WH-4 is the California DE 4 form. This form serves a similar purpose for California employees, allowing them to claim personal exemptions and additional withholding amounts. Like the WH-4, the DE 4 requires information about the employee's marital status and dependents. However, California's form includes specific instructions related to state tax laws, reflecting the unique tax structure of California compared to Indiana.

The New York State IT-2104 form also shares similarities with the Indiana WH-4. This form is used by New York employees to determine their state income tax withholding. Both forms ask for personal details and provide options for claiming exemptions. The IT-2104, however, includes provisions for additional withholding based on the employee's anticipated tax liability, which mirrors the additional withholding options found in the WH-4.

The Texas Employee's Withholding Certificate (Form W-4) is another document that aligns with the Indiana WH-4. Although Texas has no state income tax, the W-4 allows employees to claim withholding exemptions for federal taxes. Both forms require similar personal information and provide a structure for claiming exemptions, highlighting the importance of accurately reporting one’s tax status to avoid under- or over-withholding.

The Illinois Employee's Withholding Allowance Certificate (Form IL-W-4) is also comparable. This form allows Illinois employees to claim allowances that affect their state income tax withholding. Similar to the WH-4, the IL-W-4 requires personal information and provides a method for employees to adjust their withholding based on their family situation and financial needs, emphasizing the importance of personal circumstances in tax calculations.

In addition, the Florida Employee's Withholding Allowance Certificate (Form W-4) is relevant, although Florida does not have a state income tax. The W-4 allows employees to specify their federal withholding allowances. Both forms require personal data and provide a mechanism for employees to manage their tax withholding, reflecting the broader purpose of withholding certificates in various states.

The Arizona Bill of Sale form is a legal document that facilitates the transfer of ownership of personal property from one individual to another. This form serves as proof of the transaction and outlines important details such as the description of the item, purchase price, and the parties involved. For more information, you can visit https://arizonapdfforms.com/bill-of-sale, where understanding how to properly complete this form is essential for ensuring a smooth transfer and protecting both the buyer's and seller's rights.

Lastly, the Massachusetts Employee's Withholding Exemption Certificate (Form M-4) resembles the Indiana WH-4 in its function. This form allows Massachusetts employees to claim exemptions and adjust their state income tax withholding. Both forms require similar information about marital status and dependents, illustrating how state-specific forms serve the same fundamental purpose of ensuring appropriate tax withholding based on individual circumstances.

FAQ

What is the Indiana WH-4 form?

The Indiana WH-4 form is an Employee’s Withholding Exemption and County Status Certificate. It is used to inform your employer about your withholding exemptions and the county where you reside and work. This form is crucial for determining how much state and county income tax should be withheld from your paycheck. Remember, you do not need to send this form to the Department of Revenue; just return it to your employer.

Who needs to fill out the WH-4 form?

All employees who earn income subject to Indiana state and/or county income tax must complete the WH-4 form. This includes both residents and nonresident employees. If you are a nonresident alien, there are specific instructions for you, as you are only allowed to claim one exemption for withholding tax purposes.

How do I determine my exemptions on the WH-4 form?

To determine your exemptions, start by reviewing the criteria for each line on the form. You can claim one exemption for yourself. If you are married and your spouse does not claim their exemption, you can claim one for them as well. Additionally, you can claim exemptions for dependents, individuals who rely on you for support. If you or your spouse are over 65 or legally blind, you can also claim additional exemptions. Add up all the exemptions you qualify for and enter the total on the form.

What if my situation changes after I submit the WH-4 form?

If your circumstances change, such as a divorce or a change in your dependents, you must file a new WH-4 form within 10 days. This is important to ensure your withholding reflects your current situation. If your number of exemptions increases, you can file a new form at any time. Keeping your information up-to-date helps avoid any potential tax issues later on.

Can I request additional withholding on the WH-4 form?

Yes, you can request additional withholding by entering an amount on lines 7 and 8 of the WH-4 form. This allows you to specify how much extra state or county tax you want withheld from each paycheck. However, it’s important to note that entering an amount does not obligate your employer to withhold it. You remain responsible for any additional taxes owed at the end of the year.

What happens if I provide false information on the WH-4 form?

Providing false information on the WH-4 form can lead to penalties. It is crucial to ensure that all the information you provide is accurate and truthful. Misrepresenting your exemptions or other details could result in increased tax liability or other legal consequences. Always double-check your entries before submitting the form to your employer.

Common mistakes

Filling out the Indiana WH-4 form can be straightforward, but many people make common mistakes that can lead to issues down the line. One frequent error is not including the correct Social Security Number or ITIN. This number is essential for the employer to report your income accurately. If this number is missing or incorrect, it can delay processing and lead to complications with your tax filings.

Another mistake is failing to provide the correct county information. The form requires you to enter your county of residence and your county of principal employment as of January 1. If you do not live or work in Indiana on that date, you should write "not applicable." Not doing so can result in incorrect tax withholding.

Many individuals also struggle with claiming the correct number of exemptions. For instance, if you are married and your spouse does not claim their exemption, you may claim it for yourself. However, if you mistakenly enter a number greater than allowed, it can lead to under-withholding and potential tax liabilities later. It’s important to read the instructions carefully and ensure that you are only claiming what you are entitled to.

Some people overlook the section for additional exemptions. If you or your spouse are over 65 or legally blind, you can claim extra exemptions. Failing to check the appropriate boxes or miscalculating the total can affect how much tax is withheld from your paychecks. Always double-check this section to ensure you are maximizing your eligible exemptions.

Another common error involves the additional withholding amounts. Lines 7 and 8 allow you to specify extra amounts to be withheld from your paycheck. If you leave these lines blank when you actually want additional withholding, you might end up with a tax bill at the end of the year. Conversely, if you enter an amount without understanding your tax situation, you could be over-withheld, affecting your cash flow.

Lastly, many individuals forget to sign and date the form. A missing signature can render the form invalid, causing your employer to disregard it. This oversight can lead to incorrect withholding and create unnecessary headaches when tax season arrives. Always ensure that you sign and date the form before submitting it to your employer.

Indiana Wh 4 Preview

Form

State Form 48845 (R10 /

State of Indiana

Employee’s Withholding Exemption and County Status Certificate

This form is for the employer’s records. Do not send this form to the Department of Revenue.

The completed form should be returned to your employer.

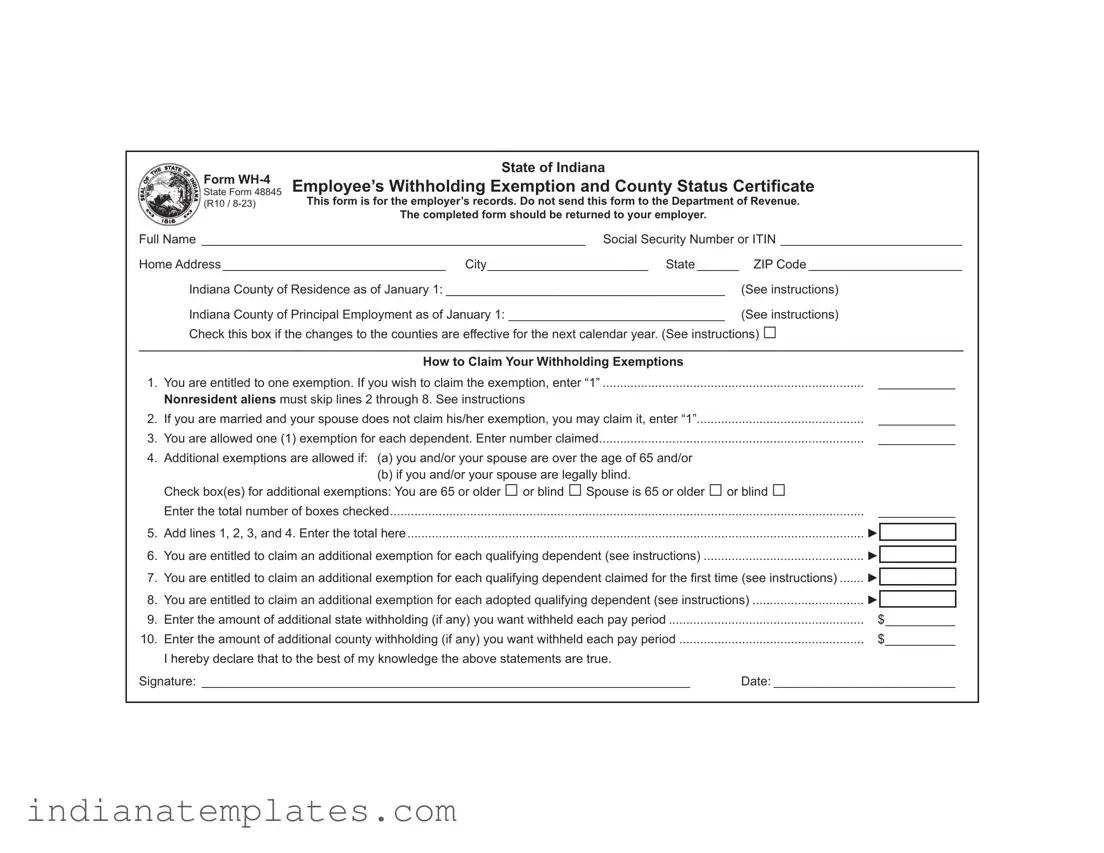

Full Name_ _______________________________________________________ Social Security Number or ITIN___________________________

Home Address_________________________________ City_______________________ State_______ |

ZIP Code_______________________ |

||||

|

Indiana County of Residence as of January 1:_________________________________________ |

(See instructions) |

|

|

|

|

Indiana County of Principal Employment as of January 1:________________________________ |

(See instructions) |

|

|

|

|

Check this box if the changes to the counties are effective for the next calendar year. (See instructions) □ |

|

|

|

|

_____________________________________________________________________________________________________________________________________ |

|||||

|

How to Claim Your Withholding Exemptions |

|

|

|

|

1. |

You are entitled to one exemption. If you wish to claim the exemption, enter “1” |

___________ |

|

||

|

Nonresident aliens must skip lines 2 through 8. See instructions |

|

|

|

|

2. |

If you are married and your spouse does not claim his/her exemption, you may claim it, enter “1” |

___________ |

|

||

3. |

You are allowed one (1) exemption for each dependent. Enter number claimed |

___________ |

|

||

4. |

Additional exemptions are allowed if: (a) you and/or your spouse are over the age of 65 and/or |

|

|

|

|

|

(b) if you and/or your spouse are legally blind. |

|

|

|

|

|

Check box(es) for additional exemptions: You are 65 or older □ or blind □ Spouse is 65 or older □ or blind □ |

|

|

|

|

|

Enter the total number of boxes checked |

___________ |

|

||

|

|

|

|

|

|

5. |

Add lines 1, 2, 3, and 4. Enter the total here |

► |

|

|

|

|

|

|

|

||

6. |

You are entitled to claim an additional exemption for each qualifying dependent (see instructions) |

► |

|

|

|

7. |

You are entitled to claim an additional exemption for each qualifying dependent claimed for the first time (see instructions) |

► |

|

|

|

|

|

||||

|

|

|

|||

8. |

.................................You are entitled to claim an additional exemption for each adopted qualifying dependent (see instructions) |

► |

|

|

|

9. |

Enter the amount of additional state withholding (if any) you want withheld each pay period |

$__________ |

|

||

10. |

Enter the amount of additional county withholding (if any) you want withheld each pay period |

$__________ |

|

||

|

I hereby declare that to the best of my knowledge the above statements are true. |

|

|

|

|

Signature:_ ______________________________________________________________________ |

Date:___________________________ |

||||

Instructions for Completing Form

This form should be completed by all resident and nonresident employees having income subject to Indiana state and/or county income tax.

Print or type your full name, Social Security number or ITIN and home address. Enter your Indiana county of residence and county of principal employment as of January 1 of the current year. If you neither lived nor worked in Indiana on January 1 of the current year, enter ‘not applicable’ on the line(s). If you move to (or work in) another county after January 1, your county status will not change until the next calendar year. Please check the box if you are requesting a change to a county of residence or work for the next calendar year.

Nonresident alien limitation. A nonresident alien is allowed to claim only one exemption for withholding tax purposes. If you are a nonresident alien, enter “1” on line 1, then skip to line 9. You are considered to be a nonresident alien if you are not a citizen of the United States and do not meet the green card test and the substantial presence test (get Publication 519 from www.irs.gov for information about these tests).

All other employees should complete lines 1 through 8.

Lines 1 & 2 - You are allowed to claim one exemption for yourself and one for your spouse (if he/she does not claim the exemption for him/herself). If a parent or legal guardian claims you on their federal tax return, you may still claim an exemption for yourself for Indiana purposes. You cannot claim more than the correct number of exemptions; however, you are permitted to claim a lesser number of exemptions if you wish additional withholding to be deducted.

Line 3 - Dependent Exemptions: You are allowed one exemption for each of your dependents based on state guidelines. To qualify as your dependent, a person must receive more than

Line 4 - Additional Exemptions. You are also allowed one exemption each for you and/or your spouse if either is 65 or older and/or blind. Line 5 - Add the total of exemptions claimed on lines 1, 2, 3, and 4. Enter the total in the box provided.

Line 6 - Additional Dependent Exemptions. An additional exemption is allowed for certain dependent children that are included on line 3. The dependent child must be a son, stepson, daughter, stepdaughter, foster child, and/or child for whom you are a legal guardian. The dependent must be under age 19 or must be both under age 24 and a

Line 7 -

Line 8 - Additional Adopted Dependent Exemptions. An additional exemption is allowed for certain dependent children that are included on lines 3 and 6 and have been adopted by you or your spouse. The dependent child must be a son, stepson, daughter, or stepdaughter. The dependent must be under age 19 or must be both under age 24 and a full- time student at a qualified educational institution during at least 5 months of the taxable year.

Lines 9 & 10 - If you would like an additional amount to be withheld from your wages each pay period, enter the amount on the line provided. NOTE: An entry on this line does not obligate your employer to withhold the amount. You are still liable for any additional taxes due at the end of the tax year. If the employer does withhold the additional amount, it should be submitted along with the regular state and county tax withholding.

You may file a new Form

(a)you divorce (or are legally separated from) your spouse for whom you have been claiming an exemption or your spouse claims him/herself on a separate Form

(b)someone else takes over the support of a dependent you claim or you no longer provide more than

(c)a dependent no longer qualifies for an additional dependent or an adopted dependent exemption.

Penalties are imposed for willingly supplying false information or information which would reduce the withholding exemption.

Different PDF Forms

Indiana Ged Transcript - Review the instructions carefully before submitting your request.

To ensure a clear understanding of the rental agreement, both landlords and tenants are encouraged to utilize resources such as the UsaLawDocs.com, which provides comprehensive information and templates for the New York Residential Lease Agreement form, thus minimizing potential disputes and enhancing the rental experience.

Indiana State 50181 - Check the appropriate boxes that apply to ensure proper processing.

St-103 - Purchasers must adhere to Indiana code to validate their claimed exemptions.